Emotions and money: how do feelings influence finances?

What is the relationship between emotions and money and how can it affect your finances?

Announcements

Emotions and money: have you ever stopped to think about what is behind your purchasing and investment decisions?

Emotional intelligence in finance is extremely important for improving financial control and making more effective decisions. However, in practice, this is not as easy as it seems.

Using your money wisely also means controlling your own feelings and impulses, which, depending on the situation, can lead to debt and worries.

With that in mind, in today's article, we're going to talk more about the relationship between emotions and money, as well as show you some ways to develop emotional intelligence in finance.

To find out more, read on.

What is emotional intelligence in finance?

Emotional intelligence in finance is basically the ability to control emotions to avoid impulsive decisions that can harm your budget.

The definition, as you can see, is something simple.

However, it is no surprise to anyone that avoiding consumerism is not so easy in practice.

After all, we are constantly bombarded with advertisements for promotions, new product launches and advertisements for goods that seem to be essential.

Additionally, companies are constantly developing strategies to get consumers to spend more.

However, it is essential to develop this control and optimize financial planning, as compulsive shopping, especially when done frequently, they snowball and cause a lot of concern.

In the financial context, emotional intelligence is related to rational money management, planning and organization.

Furthermore, the habit of giving up superfluous desires in the present, to achieve greater goals in the medium and long term, also says a lot about financial control and intelligence.

What are the pillars of emotional intelligence?

According to the psychologist Daniel Goleman, emotional intelligence can be divided into some skills, which are:

• Emotional self-knowledge: ability to recognize one's own emotions and feelings;

• Emotional control: deal with one's own feelings and control impulses, as well as make correct decisions even in times of adversity;

• Self-motivation: power to deal with frustrations and direct feelings to achieve life goals;

• Recognizing emotions in other people: recognize what the other person feels and have empathy;

• Skills in interpersonal relationships: ability and capacity to interact with other individuals.

Each of these pillars, in emotional and financial intelligence, can help you better understand the relationship between emotions, money and the way you manage your personal finances.

Emotions and money: how to develop emotional intelligence in finance

By adopting a consumer behavior capable of combining emotional intelligence with a good financial strategy, you can focus more on your goals and increase control over your spending.

However, in addition to maintaining a positive attitude, it is also necessary to identify harmful habits and make some necessary changes.

Check out some ways to use emotional intelligence in personal finances:

1. Include financial control in your routine

Financial control must become a habit in your routine.

Therefore, as important as motivation is focus and discipline.

The first step to doing this is to create a financial plan. This way, you will understand what your main income and expenses are, meaning you will know exactly where your money is going.

Ideally, you should create a spreadsheet with all your monthly expenses. This way, as we said, you will better understand your consumption habits.

The tip is to always follow your financial planning and have an emergency fund, so that you can better deal with unforeseen events.

2. Have consumption habits compatible with your income

You need to be careful with some methods that encourage consumption above your monthly income, such as credit cards, overdrafts and loans.

The credit card, for example, it is a great tool that brings practicality and security to your daily life.

In fact, if you have financial organization, it becomes an ally for your finances.

However, uncontrolled use can generate debts.

These are some signs that your standard of living is above your income:

• Have you ever taken out loans to buy non-essential products;

• You have entered the credit card revolving credit;

• Lack of an emergency reserve to deal with unforeseen events;

• You buy goods just for the status they bring;

• Your credit card is full of installments.

To have a standard of living consistent with your income, you need to plan your budget, use credit wisely and reduce household expenses.

Create goals

When you have clearly defined goals, it becomes easier to maintain discipline.

However, for everything to go as planned, you need to develop realistic goals.

Additionally, it is ideal that you set deadlines for achieving goals.

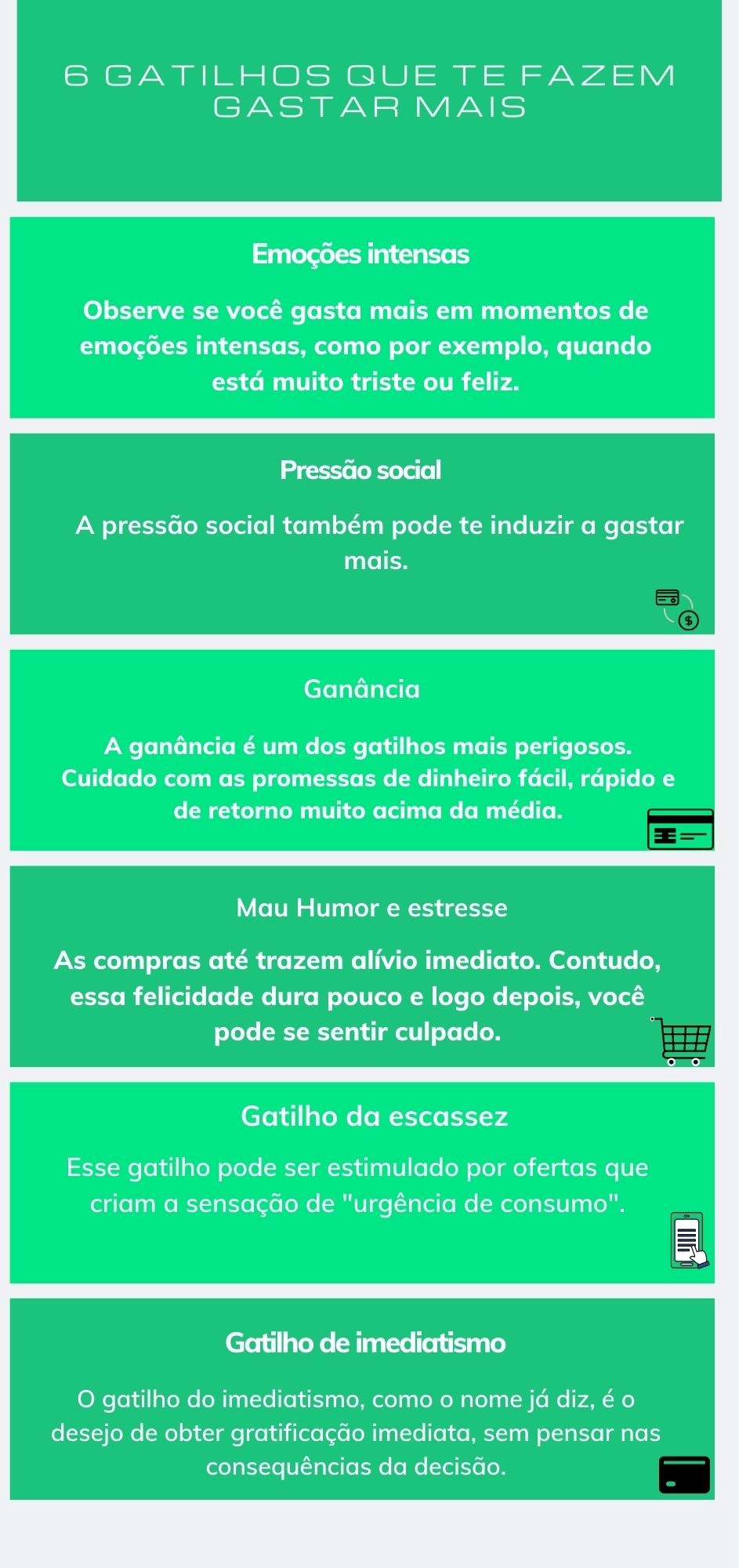

Recognize unnecessary shopping impulses

Controlling impulsive consumption is, without a doubt, one of the main skills of emotional intelligence in finance.

You've probably bought something in the heat of the moment and then regretted it because you realized you didn't need it.

To prevent this from happening again, you need to understand where these impulses come from, as this makes it easier to control them.

One tip is to avoid shopping when you are feeling very sad or happy, as this can trigger you to spend more.

Invest in your financial education

Financial education is knowledge related to money and how it works.

By investing in personal financial education, you begin to truly understand the value of money and the importance of each of your decisions.

Once you begin to master the main concepts, you will have more discipline to pursue your financial goals.

Conclusion

There is a strong relationship between emotions and money.

Understanding this is essential to setting more realistic goals, avoiding impulsive purchases and planning your finances.

So, how have you been using emotional intelligence to control and manage your finances?