8 Financial Habits That Are Ruining Your Money

There are good and bad financial habits. Often, we're so used to our routine that we don't even notice some of the habits that could be draining our money.

Announcements

These are common practices that people tend to get used to, but which in the medium and long term, have consequences.

The good news is that changing these habits is possible! But it requires discipline and motivation.

Next, see which practices could be quickly taking your money away.

1. Making small daily expenses without controlling them

It may seem silly, but the truth is that small expenses, when accumulated, make a big difference to your budget.

The problem isn't exactly making small purchases, but ignoring these expenses, which should be recorded in a spreadsheet.

The more you understand these expenses, the better you can plan!

2. Consider the overdraft as part of your income

An overdraft is a type of “automatic loan”.

In other words, it is a credit limit made available in a current account, which can be used when there is not enough balance to pay bills.

It turns out we're talking about a dangerous resource, which can give rise to one of the worst financial habits: thinking that overdrafts are part of the budget.

As much as this tool may bring momentary financial relief, it's important to remember that that money isn't yours.

This means you will have to pay it back and with high interest.

The situation often snowballs: the consumer spends more and when the salary arrives in the account, the income is already compromised due to the overdraft.

For this reason, only use your overdraft in extreme situations!

3. Not having goals for your saved money

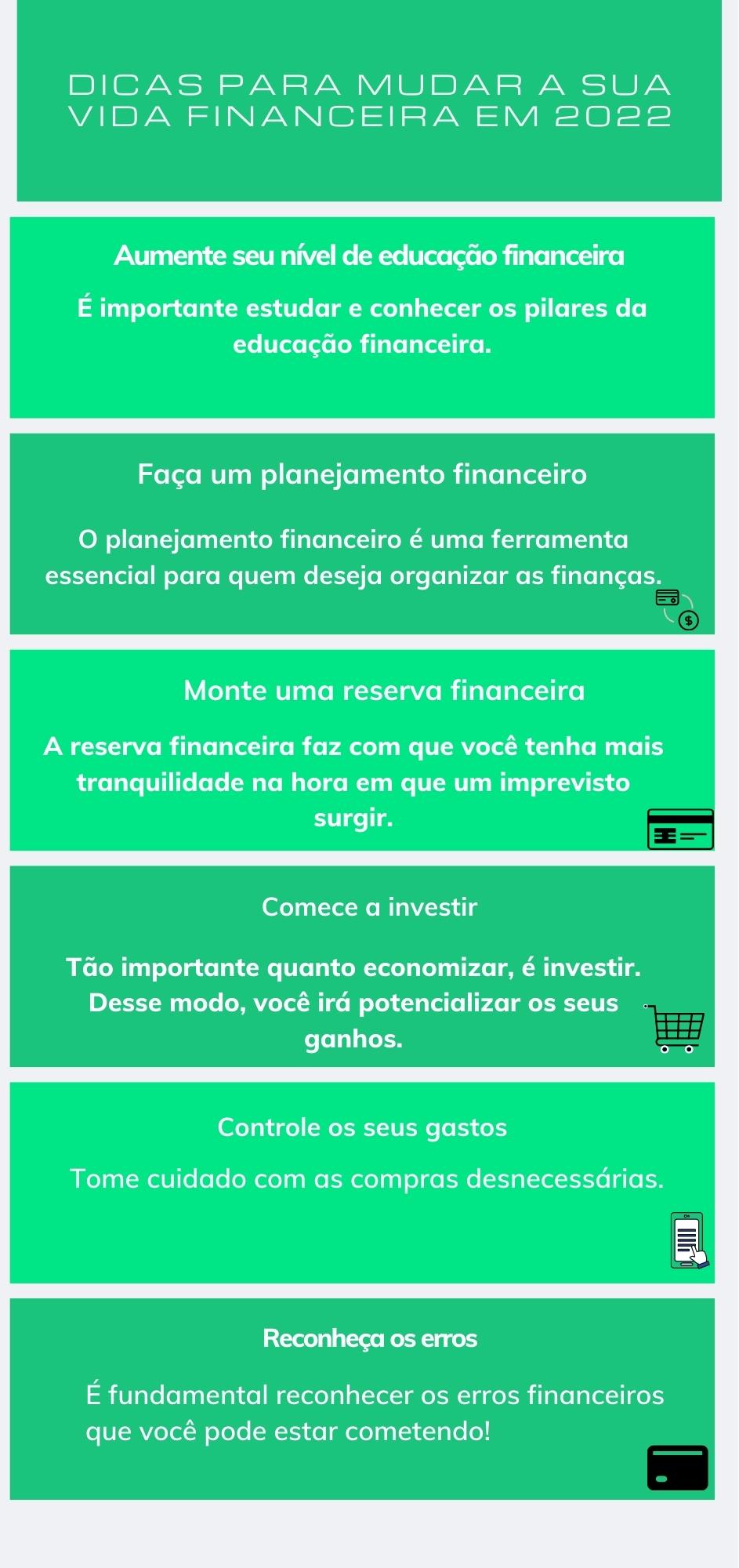

Saving is one of the main pillars of financial education.

If you're managing to save part of your income, in a way, you're already ensuring financial peace of mind in times of unforeseen circumstances.

But if you don't have a purpose for that money, at some point you might spend it on something unnecessary.

Therefore, it's important to establish your main goals. Do you want to take a trip at the end of the year? Replace your car? Build your emergency fund?

Knowing why you need to save money is essential for staying focused!

4. Not investing your money

As we said, saving is important and it is something that must be done.

However, just saving money is not enough. After all, investing is one of the other pillars of financial education.

Because of inflation, if you just save money, you will lose your purchasing power, especially if you are thinking about future, high-value goals.

Therefore, to maximize your gains in the medium and long term, it is essential to start investing.

Regarding the best type of investment, it all depends on your goals, investor profile and your risk tolerance.

5. Not having an emergency fund

An emergency fund is money saved over time to cover fixed expenses in case of unforeseen circumstances.

It should be used when a person suffers a sudden drop in income or needs to deal with an unexpected expense, such as repairing a car or appliance, for example.

This reservation It will make you feel more financially secure, because if something happens, you will be able to use the money saved.

This way, you won't need to resort to high-interest loans.

Ideally, you should put your emergency fund in a low-risk investment with daily liquidity and a yield.

A good option are digital banks, like Picpay, For example, the money you currently save in your Picpay digital wallet will yield 110% of the CDI.

It is a relatively advantageous value when compared to the returns offered by a traditional savings account.

6. Waste

Waste is one of the worst financial habits you can have.

The problem is that we don't always notice that waste occurs.

Have you, for example, ever thrown away food you forgot to eat and it's past its expiration date? Or forgotten to turn on the lights in your house?

It's things like this that can cause unnecessary increases in your bill.

Use your money wisely! Make sure you're not spending too much on things you don't need or use.

7. Impulsive buying

Impulsive purchases take your money away unnecessarily.

We've all, at some point, made an impulsive purchase. But as soon as the bill arrives, the "momentary joy" of buying something quickly fades.

To help you avoid these traps, we'll list some factors that influence compulsive shopping:

• Promotions

• Salespeople's smooth talk

• Advertisements on television and social media

Additionally, it's important to note that your emotions can also negatively influence your financial habits. Therefore, avoid shopping when you're feeling very happy or sad.

8. Paying unnecessary fees

You know those unnecessary fees that always appear on your bill, but only serve to increase your list of monthly expenses?

It's time to get them out of your life in 2022!

Paying fees for banking products you don't use, credit card annual fees, and subscriptions to services you haven't used in months can drain your money.

No matter how small the amount, remember that every saving is useful and that small expenses can snowball.

By doing this, you'll be able to eliminate unnecessary expenses. Consequently, you'll have more money left in your account, which you can use to purchase products and services that interest you, or even to make financial investments.

Conclusion

Now you know which financial habits are taking away your money unnecessarily.

It is important to have this knowledge, as this is the only way to build your emergency fund and achieve financial freedom.