5 facts you need to know about Open Banking

Want to know more about what Open Banking means? Then you're in the right place!

Announcements

Open Banking technology promises to revolutionize the financial market in Brazil and bring more benefits to the population.

Just as it was with Pix at the end of 2020, in recent months, banks have been talking a lot about Open Banking, a new development in the financial sector.

The first phase of the project was implemented in February 2021, and the second phase was implemented in August. During this phase, the institutions will share information about products, services and fees charged.

With the comparison, these companies will be able to develop improvements and more personalized solutions for customers.

If you want to understand more about the subject, continue reading!

What is Open Banking?

In literal translation, Open Banking means “open bank” or “open financial system”.

This set of processes allows the sharing of consumer information between financial institutions, helping in the development of tools and promoting dialogue between different platforms.

With the client's consent, the financial institutions may have access to banking information and services contracted by a customer of a given bank.

Currently, banks are the ones who own customer data. However, Open Banking is based on the premise that consumers should own this information.

In other words, it is the customer who decides whether to share certain data or not.

It is important to remember that all information flow will take place in a secure digital environment, in the same way as financial transactions.

How will Open Banking work?

With Open Banking, once the user authorizes, the bank in which he/she has an account will share the permitted data with other financial institutions.

The customer has the autonomy to choose what information they agree to share and with whom the data will be shared.

If he wishes, sharing can be stopped.

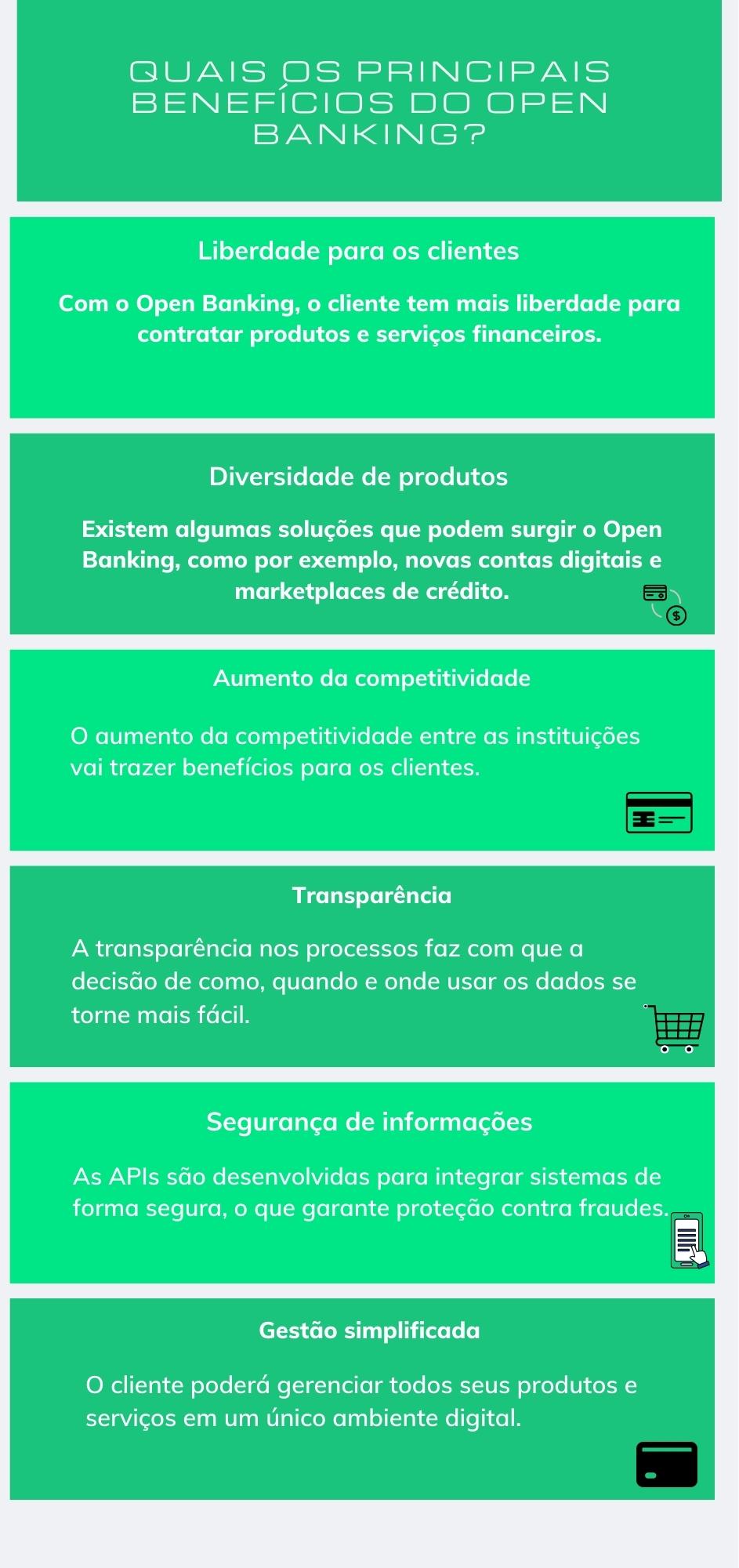

By sharing data, banks will be able to improve the user experience. With this information, users will have access to new products and more affordable costs.

Furthermore, with increased competition, financial institutions will need to develop more innovative and personalized solutions.

What you need to know about Open Banking

Everyone knows that technology has brought several benefits to the financial market!

But after all, how can Open Banking improve the user experience? What ensures that it is secure?

Below, we will show you some important facts about Open Banking so that you can better understand this set of processes. Check it out:

1. Institutions that will participate

Only institutions authorized by the Central Bank will be able to participate in the Open Banking ecosystem.

Large financial institutions are required to participate, while others can choose whether or not to participate.

Among the authorized organizations, we can mention banks, financial institutions, payment institutions and fintechs.

To consult all participants, it is just click here.

2. Data control in the hands of the customer

There has never been so much talk about customer data privacy in the digital environment.

And this is precisely one of the main objectives of Open Banking: to enable customers to better control and manage their own data.

You will be free to send information from one institution to another. This way, you will be able to access benefits and resources that are more appropriate for your financial life.

In other words, in short, the user will be able to share data from one financial institution with another.

It could be from a payment institution to a bank, for example.

The process will be carried out safely, in a modern and innovative technological environment, increasingly practical for the client.

3. Open Banking implementation phases

The schedule in Brazil is divided into four stages. Learn more about each one:

Phase 1 (Open Data from financial institutions)

It began at the beginning of 2021. It was during this phase that the Central Bank supervised the sharing of financial products and services, in addition to the rates charged by financial institutions.

It is important for you to know that customers did not participate in this phase.

Phase 2 (Consumer registration and transactional data)

The second phase began in August 2021.

Here, the customer can share some of their personal information, such as name, CPF/CNPJ and transaction data related to their account services.

Obviously, this can only happen if the consumer actually authorizes data sharing.

Phase 3 (Consumer Financial Services)

The third phase began on October 29, 2021.

It is now possible to initiate a payment outside the PIX environment. At this stage, the customer can make payment transactions in other banks.

Phase 4 (Expanding data, products and services)

The last phase is scheduled to start on 12/15.

With the implementation of the last phase, it will be possible to share other product and service data, such as information related to investments, private pensions, etc.

4. Central Bank, LGPD and banking secrecy protect customer data

As you already know, the proposal of Open Banking is to make the customer the owner of their own data, not the bank.

This is certainly one of the main concerns that you, as a customer of financial institutions, have regarding your data, isn't it?

The good news is that ensuring the security of consumer data is one of the main pillars of Open Banking in the country.

5. Data sharing authorization process

The data must be consented to by the user in the environment of the financial institution in which they wish to have access.

You will then be redirected to your current financial or payment institution.

This is where sharing confirmation occurs.

Only after completing all the steps involved will the data be shared.

Conclusion

As you can see, Open Banking allows consumers to have more autonomy, freedom and the possibility of doing business between institutions.

This entire process will help the user to have a more practical, efficient and safe experience.